|

|

|

|

March 2, 2026 |

|

What Do Outcomes Teach Us About Screening Criteria? |

|

Introduction: The Familiar Angel Tension

We look back at companies we passed on and see signs of progress: a large follow-on round, an acquisition announcement, or an IPO filing. Each one triggers the same quiet question: Did we miss something? Over time, those ghosts of past applications create pressure to loosen standards or bend rules, especially when compelling science or narratives push beyond what angel investing is designed to support.

That tension is especially familiar in life science investing. Drug, device, diagnostic, and clinically grounded digital health companies develop slowly, consume significant capital, and carry layered scientific, regulatory, reimbursement, and execution risk. Many of us invest to support better patient outcomes while also generating strong returns. But progress is not the same as success. Some companies are scientifically impressive and socially valuable, yet require too much time, too much capital, or too much dilution ever to deliver an angel-level outcome.

The Question this Analysis Sets Out to Answer

This article asks a simple but timeless question: Did Mid Atlantic Bio Angels’ (BioAngels’) disciplined screening criteria improve angel investing outcomes, or did the group miss too many of the wins that matter? To examine that question, we reviewed BioAngels’ life science application and outcome data from 2012 to 2023, covering 1,094 companies across therapeutics, medical devices, diagnostics, and a limited subset of clinically grounded digital health. BioAngels invested in roughly one percent of these applicants. Many of the companies that BioAngels declined to fund went on to raise capital from other angel groups, venture funds, or strategic investors.

While it is easier for investors to track how their investments perform, it is more difficult to analyze how companies they declined to fund have performed over time. Without that comparison, a small number of visible exceptions can create the illusion that discipline comes at the expense of returns. This review was a one-time effort to address that blind spot.

The Headline Findings

First, disciplined screening materially improves outcomes.

Second, exit quality matters far more than exit labels.

Third, true high-quality misses are rare.

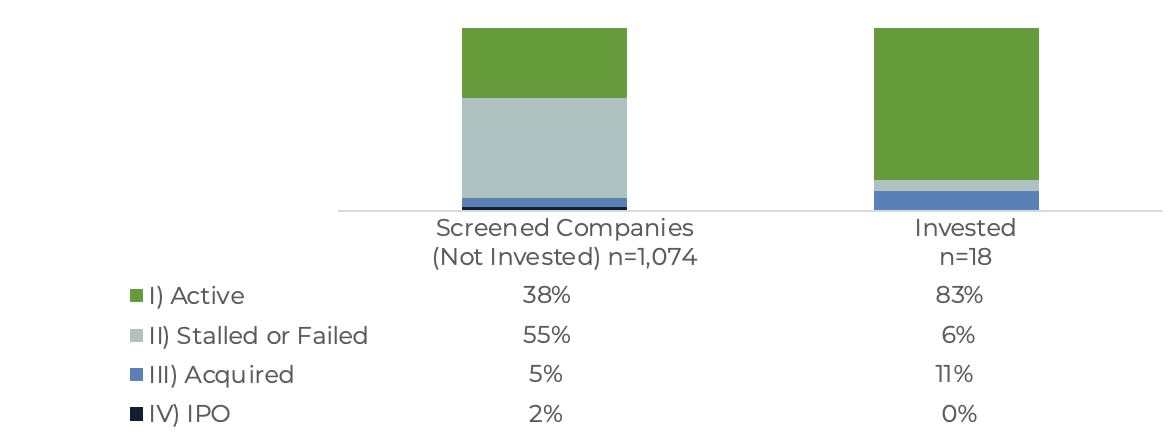

The outcomes data is also significant. Figure 1 shows that 83% of the 18 funded companies remain active, while only 38% of the 1,074 unfunded companies remain active.

Taken together, the data suggest that BioAngels’ screening criteria did more than filter activity. They improved the odds that BioAngels invested in companies capable of surviving and, in rare but critical cases, delivering outcomes that matter to angels. Screening worked because it reduced exposure to paths that destroy early-stage value, thereby increasing the odds of investing in winners. |

|

FIGURE 1. COMPANY OUTCOMES BY BIOANGELS INVESTMENT STATUS (2012–2023) |

|

|

Source: BioAngels internal analysis of life science companies that applied for funding between 2012 and 2023 (applied = 1,094; 18 funded). |

|

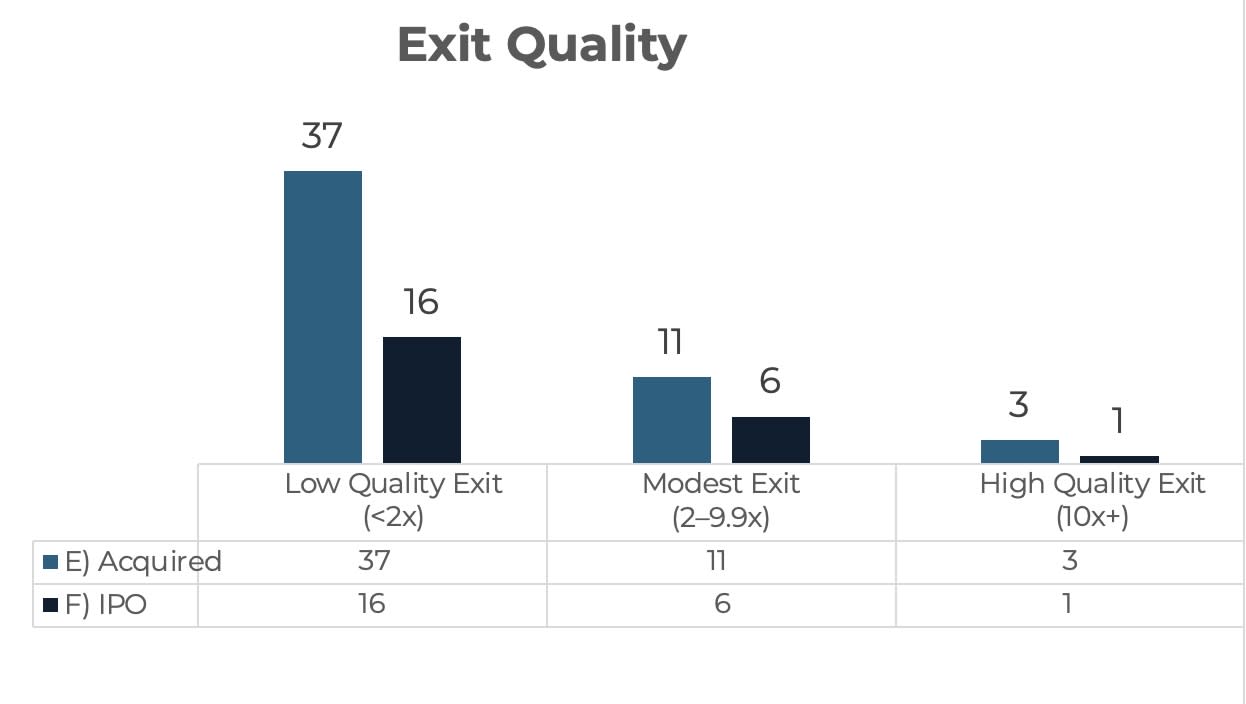

FIGURE 2. EXIT TYPE AND EXIT QUALITY AMONG OBSERVED LIQUIDITY EVENTS FOR APPLICANTS NOT FUNDED BY BIOANGELS (2012–2023) |

|

|

Source: BioAngels internal analysis of life science companies that applied for funding between 2012 and 2023 (applied = 1,094; 18 funded). Outcomes tracked using publicly available information. External sources: PitchBook, Capital IQ, ClinicalTrials.gov, FDA databases, company websites, LinkedIn, and public press releases. |

|

Screening Criteria Reflect How Angels Manage Risk

In regulated life science businesses, value creation is tightly linked to time, capital, and exit structure. Scientific, regulatory, reimbursement, and capital risks compound. When those risks are misaligned with the scale and patience of angel capital, even strong companies can produce poor outcomes for early investors. Life science companies that plan to grow all the way to standalone commercialization typically require substantial venture and public market financing over long timelines, and that combination of dilution and time often pinches angel ownership long before meaningful liquidity is reached.

BioAngels’ screening criteria begin with an expectation of what an angel-level win in life sciences looks like, as reflected in its publicly stated investment criteria. BioAngels publicly outlines its life science investment criteria, including a focus on regulated products, angel-friendly capital requirements, and exits that are “preferably by M&A,” with total capital needs typically ~$30 million or less before exit -- see BioAngels, What We Look For, available at: https://www.bioangels.org/what-we-look-for. In most cases, that win is not building a fully scaled, independent commercial company. It is being acquired at the right point, before timelines and capital requirements overwhelm early ownership.

While IPOs do occur in life sciences, they are rare sources of strong angel-level returns. Most occur before risk has been fully retired, require substantial follow-on capital, and expose early investors to extended dilution and long timelines before meaningful liquidity. There is also an expectation that a life science company that performs well in a market segment that is attractive to strategics will be acquired before it reaches a stage when it would consider an IPO. As a result, BioAngels screens IPO-driven narratives with caution and reduced enthusiasm and treats acquisition as the default, rather than exceptional, path to angel-scale success.

Across life science sub-sectors, the specifics differ, but the organizing screening questions remain consistent:

These questions play out differently by company type. Founders typically build Therapeutics companies for acquisition after Phase 1 or Phase 2, when clinical signal, mechanistic validation, and strategic fit become clear. Medical device and diagnostic companies often require regulatory clearance and early commercial traction, but not full market penetration, to become attractive acquisition targets. In all cases, the goal is not maximum growth. It is being acquisition-ready at a point in time that can be reached with angel-friendly terms and funding.

BioAngels operationalizes this thinking across four interrelated dimensions of risk, viewed through an acquisition lens.

Together, these criteria help distinguish paths compatible with angel-scale returns from those that are not. They are not rigid rules but guardrails against predictable drift. In life sciences, timelines extend, and capital requirements expand almost by default. Without discipline, companies migrate toward larger financings and longer paths to liquidity, diluting early ownership. Commercial traction can support an acquisition thesis, but only if it represents a value inflection point attractive to a strategic buyer rather than the start of a capital-intensive scaling journey better suited for venture investors. The goal is to see how scientific, regulatory, and commercial strategies align with timing and funding in an opportunity that can utilize angel-type funding to reach an exit, without requiring VC-type follow-on investments or extended timelines.

Angel-scale life science exits are often about being acquired early, not growing big.

Conclusion The group undertook this internal exercise to examine whether its criteria and best practices, which evolved over time, would be supported or refuted by retrospective data. It found that in the group’s dataset, discipline increased the likelihood that a small number of investments could produce outcomes that matter, without relying on long timelines, heavy dilution, or public-market success.

Viewed in context, the BioAngels dataset sends a clear signal in support of a specific screening and diligence strategy. Although only about one percent of applicants ultimately received investment, that selectivity reflects a deliberately narrow screening funnel. Over more than a decade of outcomes, the data show little evidence of significant misses. Very few companies that BioAngels declined to fund followed paths that produced strong angel-level returns, even when headline progress later appeared compelling, while an overwhelming majority of those that received funding remain viable.

Key Takeaways

AUTHORS

|

|

|

|

|

Contribute to Data Insights Monthly!

|

|

|

|

|

|

Angel Capital Association |